13 December 2021

Summary

Evergrande Group is an investment holding company that primarily engages in property development business in China. They are China’s second largest property company and the world’s most indebted property developer. They have liabilities of approximately over $310 billion that are set to maturity over the next 6-12 months. This implies weak recovery prospects for creditors of Evergrande if they were to default.

How did it happen?

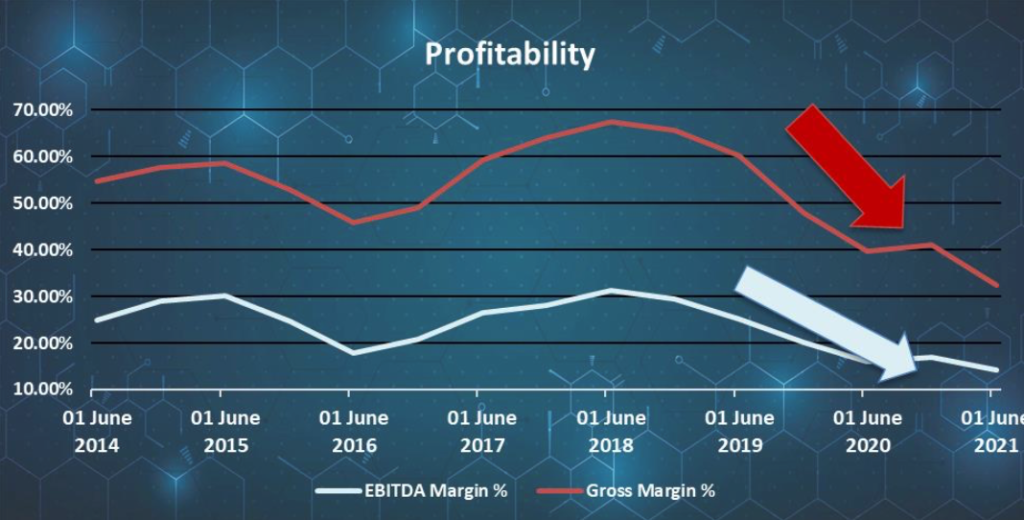

In the past, Evergrande has never reported a loss in profits and presents strong financials with consistent positive working capital in every accounting period in the company’s history.

Investors became worried about Evergrande around Q4 of 2020 when a leaked letter from the company showed that they had requested the Chinese government for support to approve a now-dropped backdoor listing plan. The company claims that the letter was a forgery.

The leaked letter consists of information regarding the company’s liabilities involving more than 128 banks and over 121 non-banking institutions. They also recently admitted that they are under “tremendous pressure” and may not be able to meet their debt obligations.

Since then, they have been downgraded by two credit rating agencies and their Hong Kong listed shares have collapsed by more than 80% this year.

In addition, Evergrande was the subject of a short seller report back in 2012. Andrew Left’s Citron Research at the centre of which lay the claim that accounting misstatements allowed Evergrande to “mask its insolvent balance sheet”. They identified 7 “red flags” that, at the time, included slowing cash collection, exploding debt and interest costs, declining presales, poor asset allocation, heavy discounting, and protests at the company’s Danyang project and press reporting of corporate restructurings and vendor payments.

At the time Hong Kong’s Securities and Futures Commission alleged that Left’s report contained “false and misleading” information on Evergrande. Hong Kong’s Market Misconduct Tribunal concluded that Left was Guilty.

Fast forward to 2021 and many of the concerns raised in Citron’s report – excessive indebtedness, access to capital markets, off balance sheet debt, poor corporate governance, poor capital allocation and liquidity issues are all at the heart of the Evergrande crisis.