Leveraged LDI and systemic risk to the UK financial services sector

06 December 2022

By Igor Tesinsky

LDI/ALM introduction

Before diving into liability-driven investing (LDI), let me explain the difference between LDI and asset-liability matching (ALM).

Historically, LDI was primarily concerned with matching the variability of liabilities with similarly variable assets. Most of the present value of pension liabilities variability stems from the market-based discount rate introduced in the IAS 19 accounting standard and pension regulations. Pension assets must be riskier than pension liabilities to achieve this matching. The second objective behind LDI was to repair scheme deficits. However, to accomplish this, assets must become even riskier.

The way to square these two objectives was to:

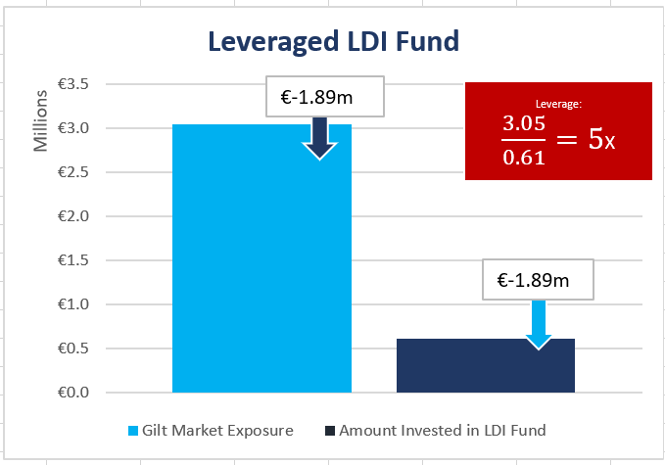

- Lever the asset portfolio

- Divide into matching and growth sub-portfolios

Leverage is achieved using Interest Rate Swaps and Repos.

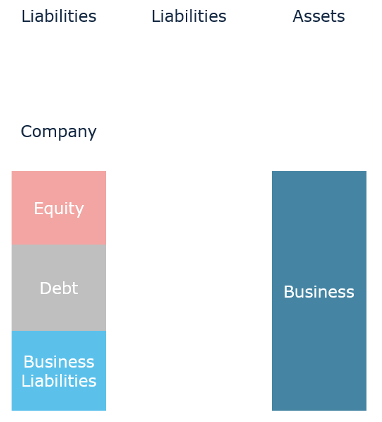

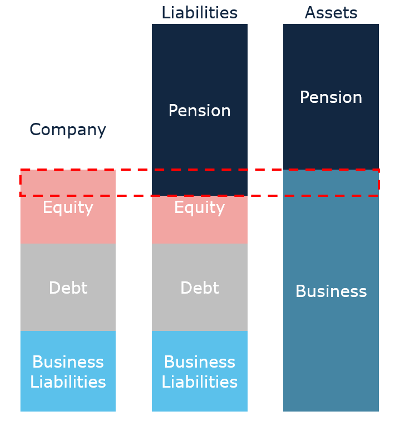

Contrary to LDI, standard ALM is concerned with protecting equity. At the sponsor/company level, assets are always greater than non-equity liabilities; hence we may match asset surplus to the non-equity to liabilities, and whatever is left, we can use to pursue growth. But the regulator (TPR) only looks at pension scheme assets and liabilities and the corresponding funding levels, ignoring the DB sponsor’s promise to pay. In other words, the Sponsor covenant is being ignored.

We believe the analysis should be of the DB scheme and company sponsor, and not just of the funding level. The regulator should look at equity exposure to the aggregate of:

- Corporate Debt

- Business Liabilities

- Pension Liabilities

and

- Company Assets

- Pension Assets

Because the regulator emphasizes the level of scheme funding based on a market-based discount rate over the valuation of the scheme and the company sponsor (sponsor covenant), the former led to artificial volatility in the valuations of pension schemes. Furthermore, the prolonged decline in rates led to excessive demand for funding (special repair contributions). The result has been leveraged LDI, as leverage limited the actual level of contributions while ensuring sufficient funding levels. Therefore LDI came about as a response to the accounting standards that introduced market-based volatility to DB pension schemes which would not be there otherwise. The first LDI was created as a response to volatility in pension scheme valuation.

What does the legislation say?

The regulations state: “the rates of interest used to discount future payments of benefits (pension liabilities) must be chosen prudently, taking into account either or both—

- (i) the yield on assets held by the scheme to fund future benefits and the anticipated future investment returns, and

- (ii) the market redemption yields on government or other high-quality bonds;”

If we recognize the sponsor covenant as an asset of the scheme, we may directly introduce the contractual accrual rate (CAR) for use as the discount rate instead of the market-based discount rate. CAR is the required rate of return on contributions (implicitly) promised by the sponsor. Unless the projected pension benefits are modified, the contractual accrual rate is invariant over time. This removes the motivation for liability-driven investment (LDI). It is also open and transparent – informing members of the contributions made and the promised investment return. Arguably, introducing a sponsor covenant means that one would need to insure sponsor default/insolvency risk, as many small sponsors will likely go out of business. Looking at empirical evidence in Germany and Sweden, the cost of such insurance is somewhere between 0.3% and 0.4% of liabilities, and that is for unfunded schemes. This option, in my opinion, is very manageable and does not create systemic risk for the UK financial sector.

Outside of possibly better solutions to DB scheme valuations, the introduction of leverage into LDI may be illegal. The LDI objectives were to ensure assets and liabilities are matched and ‘repair pension deficits’. To repair deficits, leverage was introduced via interest rate swaps and repos. This was despite DB schemes being prohibited from borrowing for purposes other than short-term liquidity under EU regulations.

- Borrowing – IORP II, Art 19

- The home Member State shall prohibit IORPs from borrowing or acting as a guarantor on behalf of third parties. However, Member States may authorize IORPs to carry out some borrowing only for liquidity purposes and on a temporary basis.

- The Occupational Pension Schemes (Investment) Regulations 2005 (OPS, 2005)

- Borrowing and guarantees by trustees

- 5.—(1) Except as provided in paragraph (2), the trustees of a trust scheme, and a fund manager to whom any discretion has been delegated under section 34 of the 1995 Act, must not borrow money or act as a guarantor in respect of the obligations of another person where the borrowing is liable to be repaid, or liability under a guarantee is liable to be satisfied, out of the assets of the scheme.

- (2) Paragraph (1) does not preclude borrowing made only for the purpose of providing liquidity for the scheme and on a temporary basis.

While leverage isn’t necessarily bad, the above suggests that it should not be introduced into DB schemes. Looking at law specifics in the UK, leverage got introduced to DB pension schemes via Pension Protection Fund (PPF), incorrectly defining Gilt repos as derivatives.

- IORP II Art 19

- (e) investment in derivative instruments shall be possible insofar as such instruments contribute to a reduction in investment risks or facilitate efficient portfolio management.

- Occupational Pension Schemes (Investment) Regulations (2005)

- (8) Investment in derivative instruments may be made only in so far as they—

- (a) contribute to a reduction of risks; or

- (b) facilitate efficient portfolio management (including the reduction of cost or the generation of additional capital or income with an acceptable level of risk),

- and any such investment must be made and managed so as to avoid excessive risk exposure to a single counterparty and to other derivative operations.

Even if we assume that the above legislation was interpreted differently to facilitate efficient portfolio management, a level of ‘acceptable leverage’ was very concerning. To illustrate, a leverage of around 4x would imply a speculative high yield rating for a corporate borrower. Still, a corporate borrower would have visibility when interest payments and/or principal become due. In the case of LDI, the pension trustee/corporate sponsor may face significant repayments (margin calls) on very short notice if Gilt rates move more significantly. While historically the interest rate changes were more gradual, bad budget decisions and/or political instability can trigger a significant shift in rates, as we witnessed in late September of 2022. Was it indeed an exceptional event considering the sharp spikes in government yields in peripheral Europe back in 2011? I don’t believe we should view a spike in government yields event as exceptional. As such, the regulator should ban/limit leveraged LDI to prevent systemic risks embedded in leveraged LDI or completely overhaul DB pension scheme regulations.

Why Levered LDI funds got into trouble?

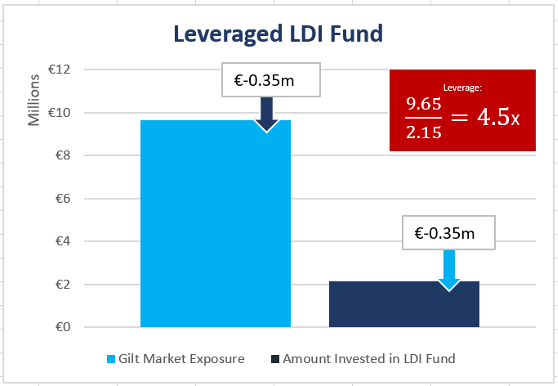

But let me explain what happened to an LDI fund in September. Let’s assume a fund has a target leverage of 4x, recapitalisation leverage of 6x (margin call) and knock-out leverage of 10x (forced liquidation of holdings).

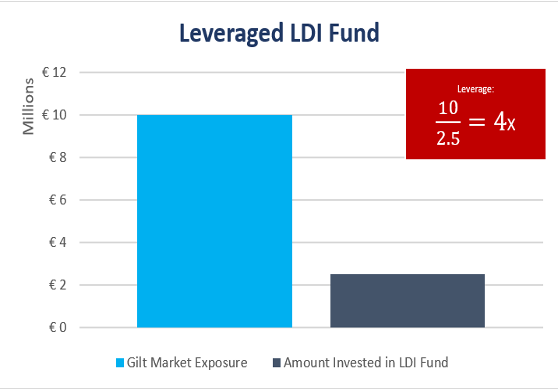

Let’s assume we want to get £10M LDI exposure, with leverage of 4x, starting on the 1st of September. We would have to invest £2.5M, as illustrated below. If Gilts value and the value of liabilities fall, the leverage of the LDI fund increases. Let’s further assume that cumulative losses on Gilts between the 1st of September and the 20th of September equalled 3.5%.

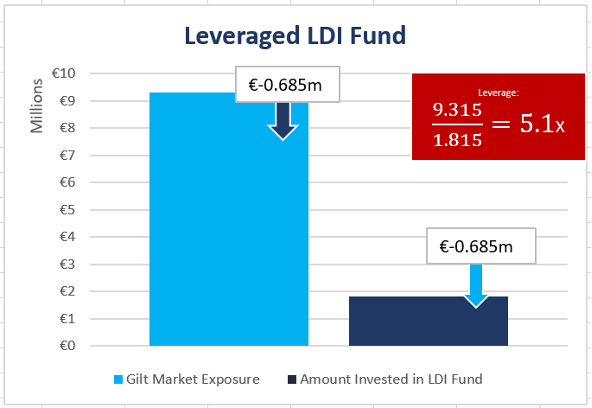

The next day, Gilt values continued falling, with the leverage of many LDI funds already somewhat elevated vs the target leverage but still manageable. Some funds have been adjusting collateral, but no significant moves in the market yet.

On the day before the mini-budget (22nd of September), our LDI fund looks like this, factoring in a slight loss since our assumed inception date. At that time, markets were nervous, anticipating the announcement may not be the one hoped for.

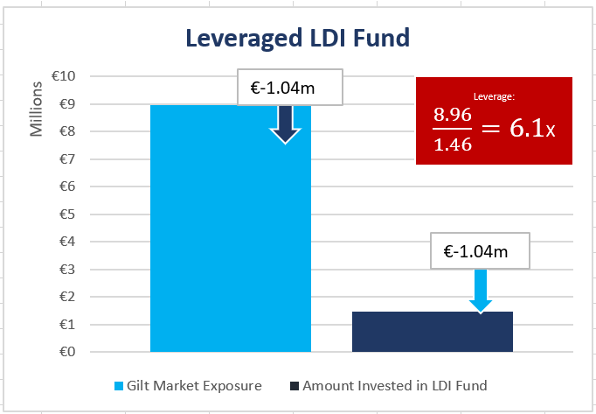

With the mini-budget announced on the 23rd of September, market concerns rose, leading to a further decline in Gilt prices and an increase in leverage. Many LDI funds have already reached recapitalization leverage and have had to submit additional collateral (margin call). In our case, a recapitalization payment of £1.2M must be made to restore our target leverage of 4x, but the pension fund trustee isn’t in a position to act quickly enough. If he could act quickly, leverage of 4x would be restored (8.96/2.24). The LDI manager is awaiting £1.2 million in collateral that is yet to arrive…

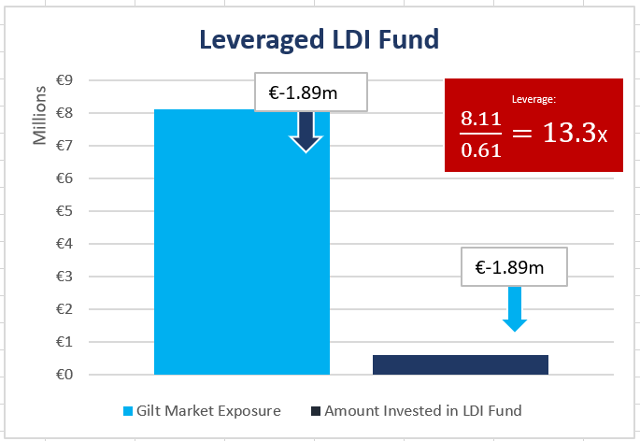

The following week, Monday, the 26th of September, the Gilt market was in a state of panic. Highly levered LDI funds were selling Gilts and other liquid assets, with conventional and index linked Gilts returning -7.18% and -8.49%, respectively, on the day. Because leverage is too high and the cash is yet to arrive, the fund manager must act immediately and sell Gilts to reduce leverage to below 6x. All LDI funds that exceeded knock-out leverage suddenly had to sell at the same time, creating a very high probability of others following the next day as there was no significant buyer that would be able to acquire Gilts after the mini-budget.

Prices of Index-Linked and conventional Gilts would continue to fall, with calls for collateral only escalating. If the Bank of England (BoE) did not step in on the 28th of September, the selling of Gilts would continue and not just the pension schemes but banks would also be in serious trouble. Not so much because of their credit exposures to pension funds under swaps but because of the effect that three days of large Gilts movements would have on their authorized regulatory capital models – three exceptions in 3 days is ‘alarming’. Technically for most banks (which operate to a hundred-day window), another two days would have invalidated those models.

So what did our model LDI fund look like right after? For example, if the fund manager targets leverage of 5x, he would have to sell £5.1M in Gilts to achieve desired leverage. This would mean lost exposure to the Gilts market of £6.95M since the Gilts sell-off started. In theory, £1.2M of additional cash should restore lost matching to some extent. However, given the significant price change following the BoE intervention on the 28th of September vs the knock-out levels that triggered selling, Gilts exposure would likely be much lower than the original £10M. As a result, the scheme lost a fair chunk of its assets and asset-liability matching because the entry point for an additional £1.2M investment would likely differ materially vs the knock-out Gilt prices.

While large pension schemes have been able to bring in incremental collateral quickly, the smaller ones that invest primarily via pooled funds probably took some time as the prospectuses allowed them to do so. The question is who should be responsible for losses. In my opinion, it depends on the prospectus. Suppose a scheme was willing to provide collateral within a certain allowed period whilst the fund manager liquidated exposure. In that case, there should be a strong case for the scheme to recover losses. We’re yet to see whether some fund managers end up facing litigations….

Conclusion

In conclusion, interest rates (discount rates) are inconsequential in determining pension benefits ultimately payable by a DB scheme, but they determine a trajectory or amortization schedule for liabilities. The interest rate risk is perceived but not a real risk in the context of DB schemes. These rates merely determine a present value for future benefits. Their variability doesn’t matter unless we base decisions and actions upon them, as with LDI. If, instead, CAR was used to evaluate the DB pension scheme and we would consider sponsor covenant, interest rate volatility wouldn’t matter. We would, however, introduce credit/default risk associated with a sponsor. That said, sponsor credit risk can be insured with the overall cost of such insurance not exceeding 0.4% of liabilities, looking at the examples of Germany and Sweden. In my opinion, implementing the latter would mean that the UK financial system would not face the systematic risk associated with levered LDI.

How Intellibonds can help?

At Intellibonds, we’re trying to help DB schemes optimize their fixed income portfolios and match assets with liabilities at these difficult times. While investing in cash or bonds may not deliver a perfect match, our intelligent software will provide custom solutions that limit the need for derivatives outside of essential hedging. Intellibonds’ AI-augmented platform can help you create the most efficient bond portfolio within minutes when constructing or rebalancing those portfolios while also predicting credit risk. Please reach out to us here. Elevated yields in the Gilt market and corporate Credit represent a unique opportunity for schemes and other long-term investors to lock in yields not seen since the 2008/9 global recession and ensure that assets will meet, if not exceed, future benefits payable.

I would like to thank Dr Con Keating for his consultation and insights. Con, it was my pleasure to discuss LDI and explore the way forward towards more stable and transparent outcomes for DB schemes.